As the Middle East conflict continues, further escalation of fertilizer price and availability issues is the latest pressure added to the farm economy, adding immense stress to an already bleak outlook for corn farmers in 2026. More and more, farmers are encountering volatile fertilizer markets, along with uncertainty about the availability of essential fertilizers – not only for 2026, but increasingly for 2027.

To empirically quantify how this developing situation may shape farmer decisions on financial and agronomic management for their operations and, ultimately, planted acres and production, the National Corn Growers Association gathered grower insight through two surveys: (1) a contracted survey of corn farmers across the country conducted by Farm Journal March 23–31 that captured nearly 1,000 farmer responses; and, (2) a survey of NCGA members conducted March 27–April 3 with more than 600 responses. Both surveys were conducted through structured, reproduceable online forms, collecting quantifiable data directly from a representative sample of farmers with less than +/- 5% margin of error at a 95% confidence level.

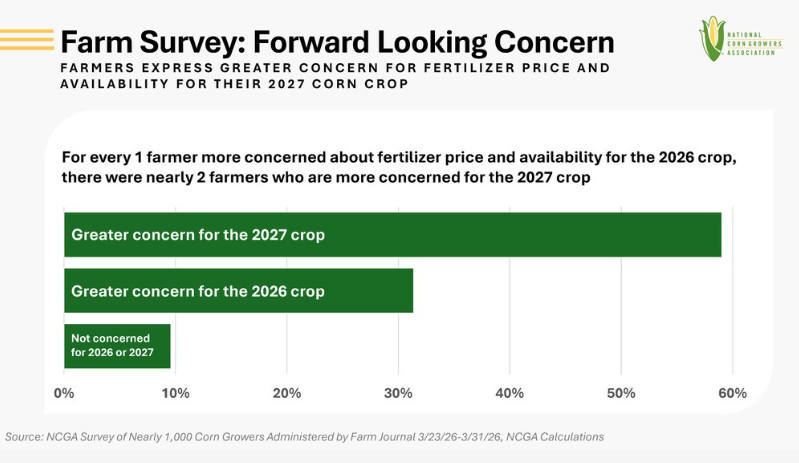

In a normal farming cycle, budgets and input purchases for next year’s crop are made during the current crop year. This means that many farmers secured some or all their fertilizer needs for this year’s planting season before the Strait of Hormuz closure increased prices. However, while the situation will still affect some corn growers this season, the uncertain nature of today’s incredibly volatile fertilizer markets is already fueling broader concern about costs and supplies for the 2027 crop. Results from NCGA surveys show that for every one farmer expressing greater concern about fertilizer price and availability for the 2026 crop, there were nearly two farmers expressing greater concern for the 2027 crop.

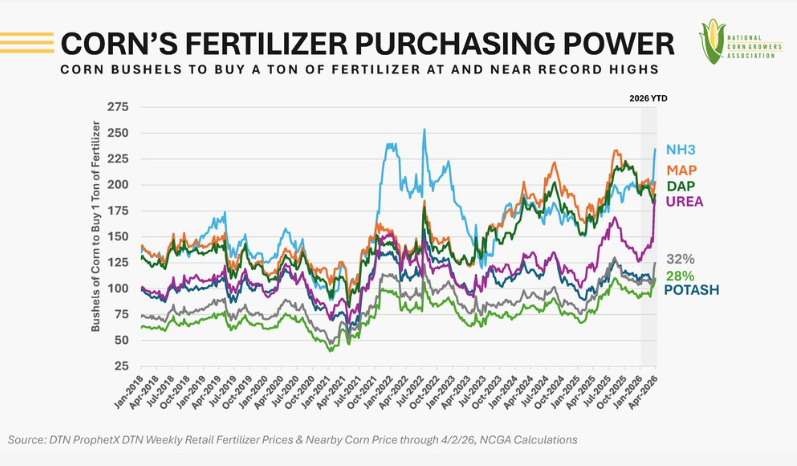

Retail Fertilizer Prices Rise, Hitting Record Highs Relative to Corn

Spot and futures prices for key fertilizers spiked immediately at the start of the conflict, reflecting the Middle East’s outsized role in global trade: the region accounts for an estimated 40-50% of international seaborne fertilizer trade of urea, and one-third of total global seaborne fertilizer volumes pass through the Strait of Hormuz.

U.S. retail prices initially lagged the futures trade, but the prices farmers pay have since increased rapidly. While still below 2022 price peaks, affordability is worsening as fertilizer prices rise relative to corn prices. On a ″currency of corn″ basis, growers now need a record 185 bushels of corn to buy one ton of urea, despite urea still retailing below peak 2022 levels, because corn is around $4.50 per bushel today, versus more than $8.00 per bushel then.

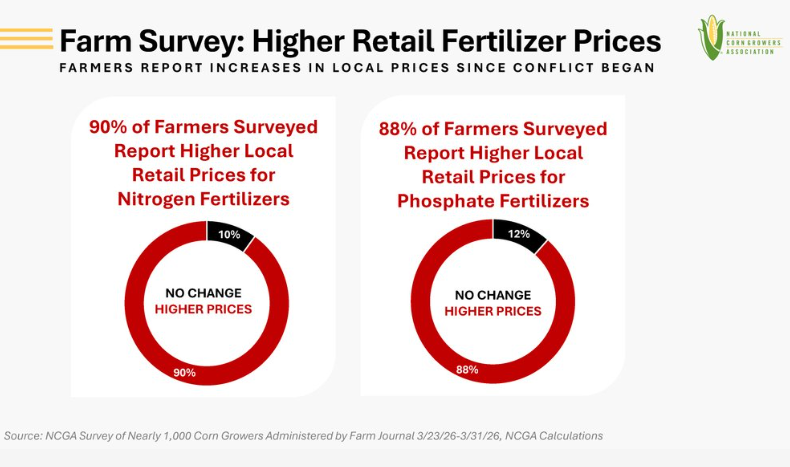

Urea, representing two-thirds of fertilizer shipments moved by sea from the Persian Gulf, has posted the largest increase since the conflict began, up 37% ($227/ton) at retail according to the DTN retail fertilizer price index. The DTN national average retail fertilizer prices for other nitrogen fertilizers are up 20-23%, and 90% of surveyed farmers report higher nitrogen prices at their local retailer.

Phosphate products have moved relatively less since the end of February in response to the conflict: DAP is up 1.2% ($10/ton) and MAP 4.2% ($37.ton). It is important to note that MAP and DAP were already at sustained elevated prices prior to the conflict due to tight supply conditions and countervailing duties in place since early 2021. However, given that DAP and MAP account for nearly 30% of the seaborne fertilizer shipments from the Persian Gulf region, further retail price pressure is possible if disruptions persist; nearly one-third of surveyed farmers report local phosphate price increases of at least $50/ton.

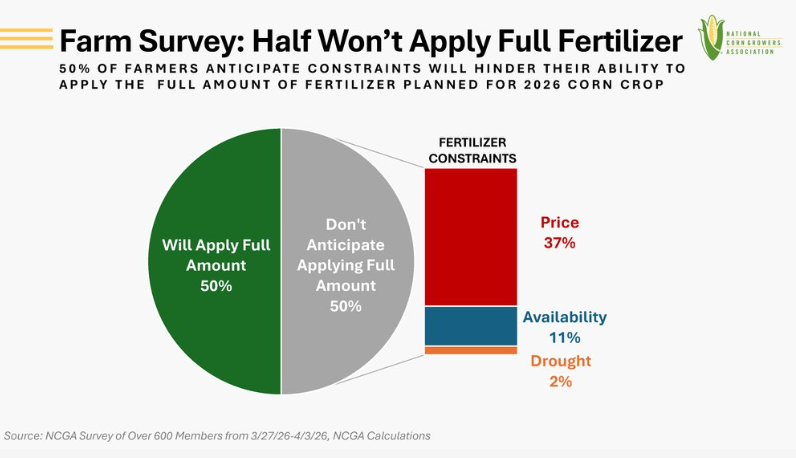

Despite higher prices, half of NCGA members surveyed do not anticipate issues applying their full planned fertilizer rate for the 2026 crop. Among the other half, 36.7% cite price as the primary constraint, 10.7% cite availability, and 2.4% cite drought conditions.

Mounting Tension Between Fertilizer Affordability and Availability

As the survey results indicate, fertilizer concerns extend beyond affordability to include availability. The volume of daily transits through the Strait of Hormuz is running about 95% below the month before the conflict, keeping supplies from flowing to the global market. Availability risks are also being reinforced by reports of curtailed fertilizer and input production in multiple locations, including Qatar, India, and Bangladesh. Decreased production capacity threatens to strain already-tight supply and demand fundamentals for a longer duration of time. At the same time, the market is pricing in a ″war premium″ even for U.S. produced product already on hand for spring application, reflecting efforts to prevent supplies from being pulled into export channels.

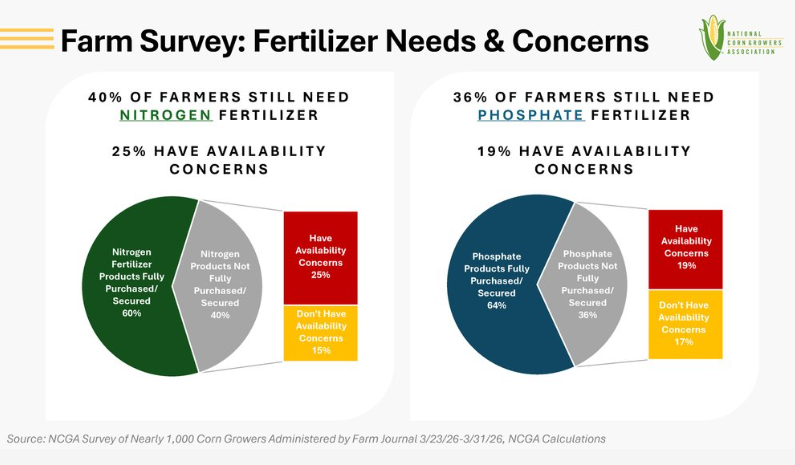

For the 2026 crop, 60% of farmers report having their nitrogen fertilizer needs fully purchased or secured; among the remaining 40% who are not fully locked in, 25% are concerned about availability. For phosphate fertilizers, 64% of farmers have fully purchased or secured needs; among the remaining 36%, 19% report availability concerns.

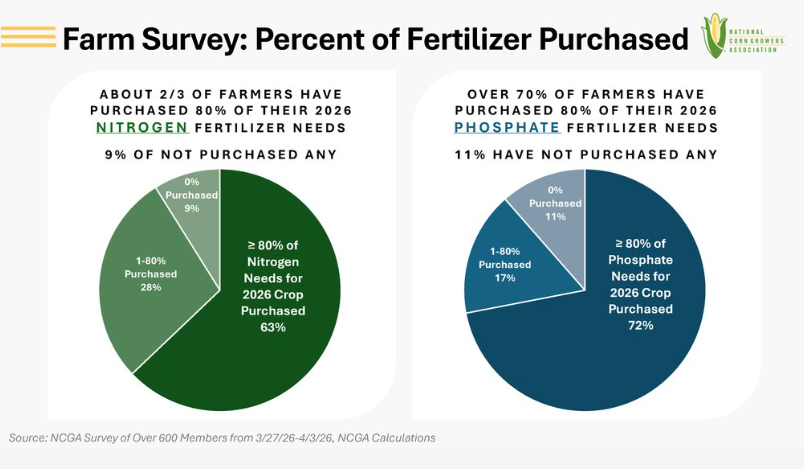

Nearly two-thirds of NCGA members surveyed have purchased at least 80% of their nitrogen needs for 2026, while 9% haven’t purchased any, representing a meaningful number of farmers, with a disproportionate share among younger producers. Respondents under 40 were more likely than other age groups to report having no nitrogen purchased.

More than 70% of NCGA members surveyed have purchased at least 80% of their 2026 phosphate needs. About 12% report having purchased none of their 2026 phosphate needs, but that share still represents a substantial number of farmers.

Limited Reported Shifts in 2026 Corn Acres

There has been speculation that conflict-driven impacts on fertilizer affordability and availability could shift acres away from corn to crops that require less fertilizer, such as soybeans. USDA’s model-based projection, released before the conflict began, estimated 94.0 million corn planted acres in 2026, down 4.8 million acres from last year. Later, USDA’s survey-based planting intentions report, derived from farmer surveys in early March, suggests farmers will plant 95.3 million acres of corn.

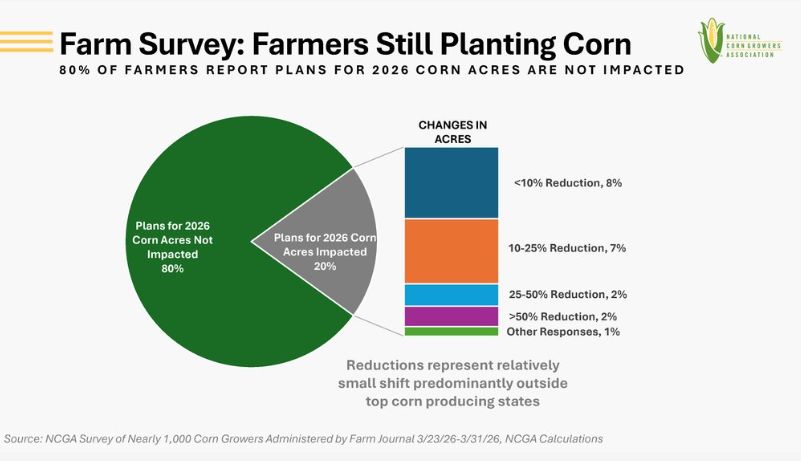

Results from nearly 1,000 farmers surveyed in the final week of March indicate limited reported changes in their plans so far: 80% said their 2026 corn acreage intentions have not been affected by the Middle East conflict. This is not surprising given the number of farmers who report having fertilizer needs locked in for 2026: if farmers had already purchased or applied fertilizer with the intention of planting corn this spring, planting a different crop would mean previously purchased or applied fertilizer will become a wasted expenditure for crops with other nutrient needs. Among those reporting a change, 88% expect to plant another crop rather than leave land unplanted. This indicates that, for 2026, fertilizer-related uncertainty is influencing crop mix at the margins more than reducing overall planted acres. For the 20% making changes, anticipated reductions are relatively low, with 8% planning to reduce corn acres by less than 10% and 7% planning to reduce corn acres by 10-25%, leaving only 5% anticipating larger reductions. Reported shifts in plans are smaller in top corn-producing states and larger in fringe production areas. In short, 2026 corn acreage expectations appear largely intact, with only incremental reallocation away from corn rather than widespread acreage loss. Reduced fertilizer applications could have implications for productivity as well.

Forward Supply Risk: Compounding Disruptions Carry into 2027 Crop Cycle

A combination of disrupted transportation and curtailed production is tightening global fertilizer supply, with implications that extend beyond the 2026 season into 2027. Persian Gulf shipments to the U.S. typically require roughly 30-45 days in transit, which means product arriving in March and early April likely cleared the Strait of Hormuz before the conflict began. While March data is not yet available, the timing suggests March urea volumes bound for New Orleans were largely insulated from the initial disruption. March and April are often peak months for fertilizer imports, driven in part by urea. Higher than normal urea imports in February 2026 may further cushion near-term effects of the Iran conflict’s impacts on April.

Phosphate exports from the Middle East are also experiencing the same disruptions as nitrogen. Currently, 39% of the United States’ phosphate imports are from Saudi Arabia and thus must use the Strait to access global markets. Unfortunately, the high countervailing duties applied to Moroccan phosphate, at the request of U.S.-based phosphate producers, have prevented a pivot to other sources for phosphate in lieu of Middle Eastern producers. These duties mean farmers are more exposed to phosphate supply chain disruptions from the Strait of Hormuz closure.

Looking ahead, risk shifts to the late-summer and fall import window, generally August through November. Volumes arriving in August would typically be produced and loaded in late spring to early summer, so today’s transit backlogs and production interruptions can compound into reduced availability even after active conflict ends.

Farmers plan inputs well ahead, and survey responses reflect the forward-looking concern: for every one farmer expressing greater concern about fertilizer price and availability for the 2026 crop, there were nearly two farmers expressing greater concern for the 2027 crop.

If import volumes remain constrained while global risk stays elevated, temporary disruptions, and existing policy-drive constraints could translate into a much bigger challenge impacting all corn growers in 2027.

Why It Matters: Fertilizer markets have tightened since the Middle East conflict began, pushing retail prices higher and worsening affordability even where prices remain below 2022 peaks. In corn terms, growers now need a record 185 bushels to purchase one ton of urea, reflecting fertilizer price increases paired with much lower corn prices. Survey results suggest many farmers can still meet most 2026 nutrient needs, but concerns about both price and supply escalate sharply for 2027 as import timelines, disrupted production, and elevated risk premiums compound over time. To avoid 2027 becoming an availability problem as well as an affordability problem, solutions that improve supply resilience and keep product moving to U.S. farms are needed before the next major purchasing and import window.

Source: National Corn Growers Association